Early December 2022, the Financial Accounts of the United States Z.1 report by the Federal Reserve showed that US household wealth fell by $400 billion in the third quarter. It is the third consecutive quarter in which household wealth has plummeted, with September data showing it slipping to $143.3 trillion from $143.7 trillion at the end of June.

Overall, American households have lost around $6.8 trillion over the first three quarters of 2022. It is the second largest drop on record, for data series starting from 1959.

High inflation increases the cost of debt, as lenders charge higher interest rates. It raises borrowing costs forces business owners to cut back on expansion plans and hurting the economy.

American household wealth drops consecutively for three quarters

Liabilities rose by about $900 billion as US household income continued to slide while expenditure soared. As the economic slowdown worsens, customers have been forced to tighten household budgets.

According to WION, these contractions in household wealth indicate that a recession is setting in place.

Effect of Inflation

The Consumer Price Index (CPI) measures price change (or inflation) faced by consumers. The CPI for December 2022 will be released by the US Bureau of Labor Statistics (BLS) in mid-January.

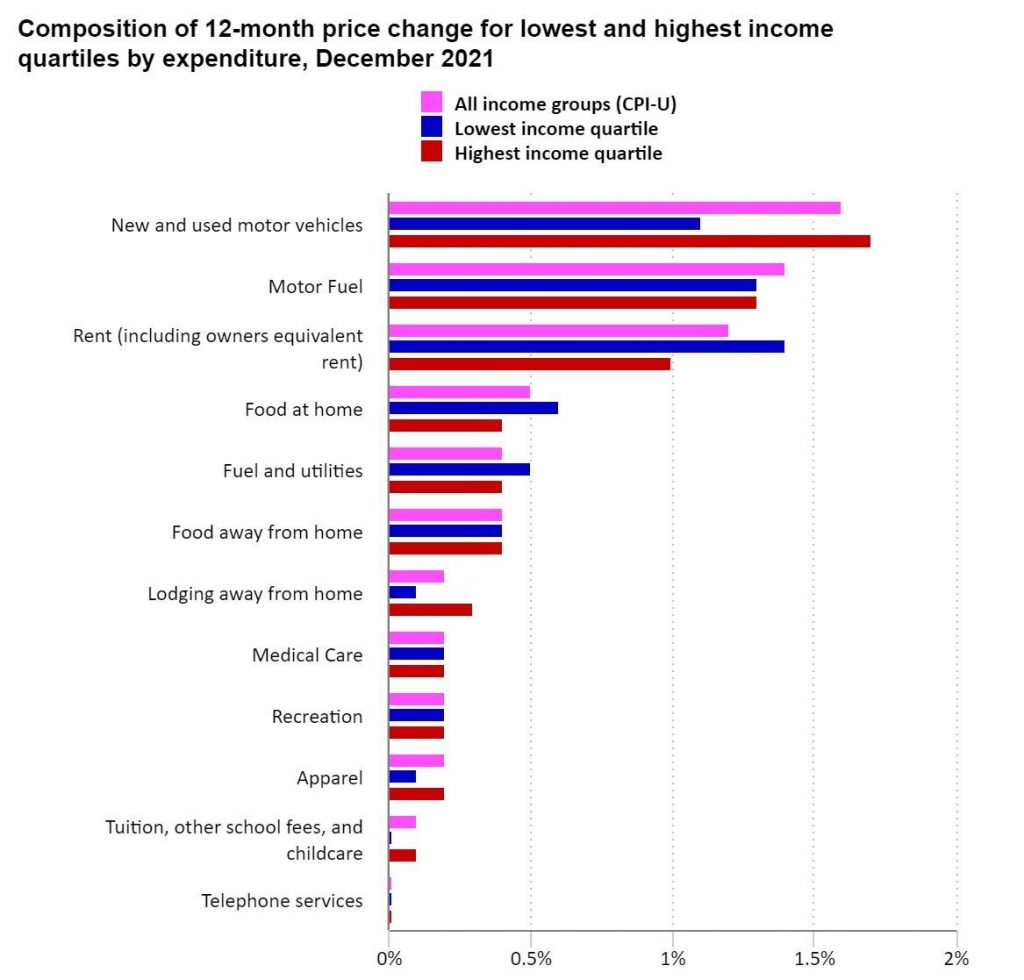

Research shows us how households with different incomes experience inflation differently.

Households with higher income usually have a higher budget for discretionary spending like traveling and entertainment. On the other hand, households with lower income spend more money on food, medical care, and rent.

BLS found that because of such differences, lower income households face higher inflation rates compared to all urban households, while highest income households face lower inflation than all urban households.

The difference in effect of inflation rates is especially high while comparing spending changes between households with highest and lowest income. While studying data between 2005 to 2020, this figure stood at 0.41 percentage points.

The record high inflation also chipped away at nominal net worth. In economics, nominal net worth refers to the unadjusted value of assets with accounting for premiums or deductions. Overall, nominal net worth fell by 4%, and market value of assets dropped by $6 trillion. Liabilities soared by $900 billion.

“Even with the likelihood that inflation has peaked, inflation will still remain elevated for some time, as supply chain issues persist and there is still plenty of instability with the Ukraine war, which has caused significant swings in energy prices,” Zach Stein, chief investment officer at investment advisory firm Carbon Collective, told Time .

A Bloomberg report stated that the US will face a recession this year.

High Inflation Erodes Real Wealth

Household balance sheets were also affected by a 10% increase in home equity. However, the real loss in household wealth from January to September was twice as big as the nominal loss. It stood at a staggering $13.5 trillion, after accounting for the rapid level of inflation in 2022.

Household balance sheets = assets minus liabilities.

Overall, there is an 8.6% drop in real wealth over three quarters of 2022. The only greater decline on record is during the financial crisis of 2008-09.

Although real household wealth was about 10% higher than it was in late 2019, the rise in household debt has raised concerns. Real household debt grew at an annual rate of 4.3% in Q3, its steepest climb since 2007.

Consumers have started dipping into savings or taking on debt to maintain their current lifestyle. According to a Fed report personal savings rate has fallen to 3.7% of disposable income, after averaging 10% for the last decade.

In aggregate households still have plenty of cash and when studied side by side have enough money to pay off all the debt taken. But the households with cash and the ones with debt are not the same. Lower income households have found their wealth declining due to Fed interest rate hikes and inflation.

How to get household income back on track?

To get real wealth back on track, we need to track spending. One must play smart to control inflation 2023.

“We are emotionally driven, getting us in trouble,” says Ashley Folkes, an Alabama-based Certified financial planner (CFP). “Fear of retirement, debt, the stock market, and inflation can certainly create fear, but we can’t let it paralyze us.”

To better understand how inflation has impacted your household, experts recommend comparing the budgets of the first four months of 2021 with 2022.

While rising interest rates and a falling stock market can induce panic, experts suggest holding on to your sanity by having a diverse investment plan.

Working out what to reduce or cut off from your budget will help you deal with the stress. Furthermore, look for ways to increase your active and passive income, to tide over the tough times.

It is unclear how much saving a typical American family has that will help it get through tough times. The Fed’s Survey of Consumer Finances report which is scheduled to release this year is expected to give a better idea on real household wealth.

Until then, households must cut corners as the Fed tries to rein in runaway inflation. But extreme erosion of wealth will inevitably lead to a recession.